In my post last week, "Agriculture and the Oil Supply," I linked this Jeremy Grantham - CIO of GMO Capital report. This outlook of Grantham's has had the blogosphere all abuzz and I do encourage you to read the whole thing if you haven't already. (Doomer Porn warning!)

Today, I will excerpt the part about agriculture, as Grantham's outlook is quite interesting, especially for those of us whose main concern is how to plan smartly for feeding the world during a coming time period of higher priced energy in an oil production constrained world.

My own view is that there is somewhat more resiliency in the Ag/Food system in the near-term, at least, than Grantham expresses, but that depends upon where you live and what our oil price and availability time frame plays out to be.

K. McDonald

“The Great Paradigm Shift.”

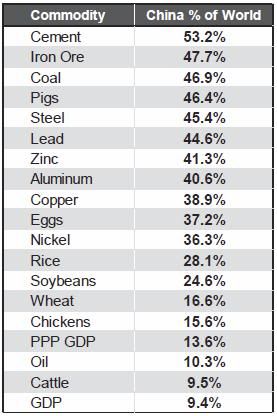

The primary cause of this change is not just the accelerated size and growth of China, but also its astonishingly high percentage of capital spending, which is over 50% of GDP, a level never before reached by any economy in history, and by a wide margin. Yes, it was aided and abetted by India and most other emerging countries, but still it is remarkable how large a percentage of some commodities China was taking by 2009.

Exhibit 3 shows that among important non-agricultural commodities, China takes a relatively small fraction of the world’s oil, using a little over 10%, which is about in line with its share of GDP (adjusted for purchasing parity). The next lowest is nickel at 36%. The other eight, including cement, coal, and iron ore, rise to around an astonishing 50%! In agricultural commodities, the numbers are more varied and generally lower: 17% of the world’s wheat, 25% of the soybeans (thank Heaven for Brazil!) 28% of the rice, and 46% of the pigs. That’s a lot of pigs!

China's Share of World Commodity Consumption (Exhibit 3)

Source: Barclays Capital 2010, Credit Suisse 2010, Goldman Sachs, United States Geological Survey 2009, BP Statistical Review of World Energy 2009, FAO 2008, IMF 2010

Optimists will answer that the situation that Exhibit 3 describes is at worst temporary, perhaps caused by too many institutions moving into commodities. The Monetary Maniacs may ascribe the entire move to low interest rates. Now, even I know that low rates can have a large effect, at least when combined with moral hazard, on the movement of stocks, but in the short term, there is no real world check on stock prices and they can be, and often are, psychologically flakey. But commodities are made and bought by serious professionals for whom today’s price is life and death. Realistic supply and demand really is the main influence.

[...]

Agricultural Commodities

Moving on to agriculture, the limitations are more hidden. We think of ourselves as having almost unlimited land up our sleeve, but this is misleading because the gap between first-rate and third-rate land can be multiples of output, and only Brazil, and perhaps the Ukraine, have really large potential increments of output. Elsewhere, available land is shrinking. For centuries, cities and towns have tended to be built not on hills or rocky land, but on prime agricultural land in river valleys. This has not helped.

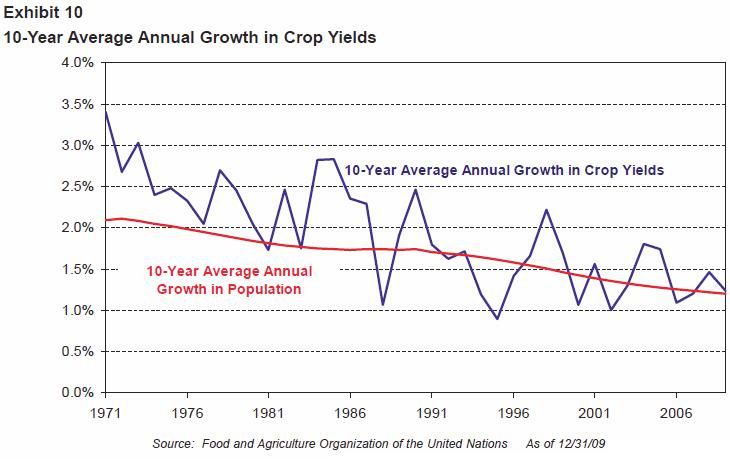

We have, though, had impressive productivity gains per acre in the past, and this has indeed helped a lot. But, sadly, these gains are decreasing. Exhibit 10 shows that at the end of the 1960s, average gains in global productivity stood at 3.5% per year. What an achievement it was to have maintained that kind of increase year after year. It is hardly surprising that the growth in productivity has declined.

It runs now at about one-third of the rate of increase of the 1960s. It is, at 1.25% a year, still an impressive rate, but the trend is clearly slowing while demand has not slowed and, if anything, has been accelerating. And how was this quite massive increase in productivity over the last 50 years maintained? By the even more rapid increase in the use of fertilizer.

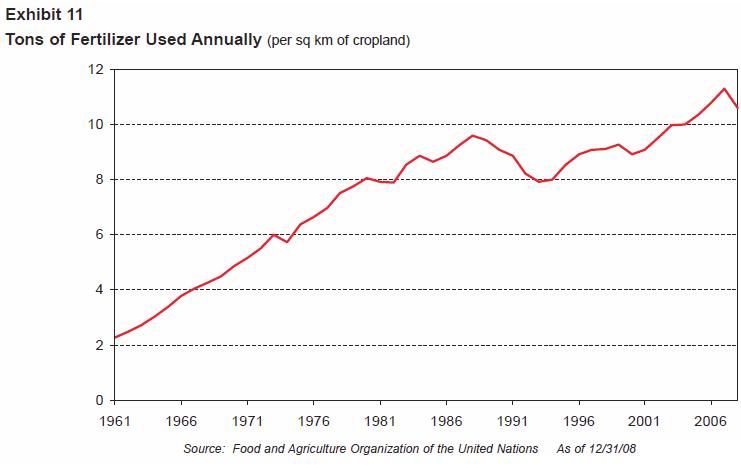

Exhibit 11 shows that fertilizer application per acre increased five-fold in the same period that the growth rate of productivity declined. This is a painful relationship, for there is a limit to the usefulness of yet more fertilizer, and as the productivity gains slow to 1%, it bumps into a similar-sized population growth. The increasing use of grain-intensive meat consumption puts further pressure on grain prices as does the regrettable use of corn in ethanol production. (A process that not only deprives us of food, but may not even be energy-positive!) These trends do not suggest much safety margin.

The fertilizer that we used is also part of our extremely finite resources. Potash and potassium are mined and, like all such reserves, the best have gone first. But the most important fertilizer has been nitrogen, and here, unusually, the outlook for the U.S. really is quite good for a few decades because nitrogen is derived mainly from natural gas. This resource is, of course, finite like all of the others, but with recent discoveries, the U.S. in particular is well-placed, especially if in future decades its use for fertilizer is given precedence.

More disturbing by far is the heavy use of oil in all other aspects of agricultural production and distribution. Of all the ways hydrocarbons have allowed us to travel fast in development and to travel beyond our sustainable limits, this is the most disturbing. Rather than our brains, we have used brute energy to boost production.

Water resources both above and below ground are also increasingly scarce and are beginning to bite. Even the subsoil continues to erode. Sooner or later, limitations must be realized and improved techniques such as no-till farming must be dramatically encouraged. We must protect what we have. It really is a crisis that begs for longer-term planning – longer than the typical horizons of corporate earnings or politicians.

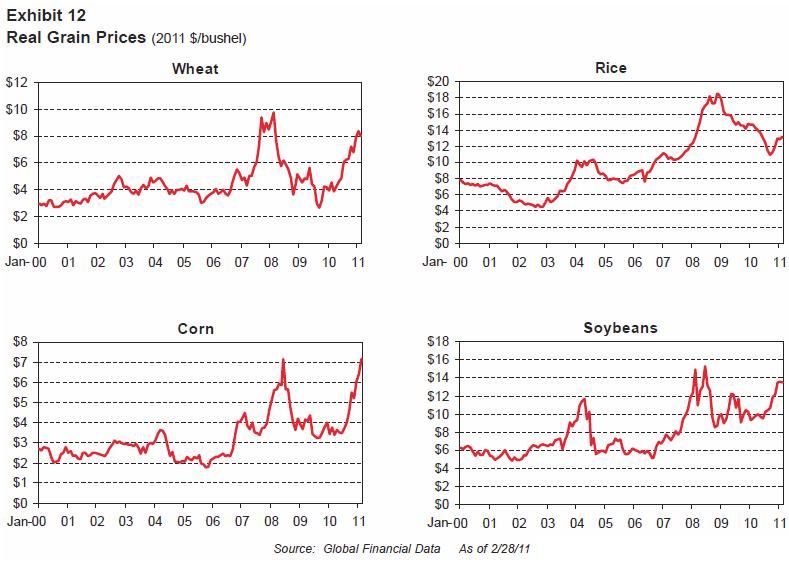

The bottom line is, as always, price, and the recent signals are clear. Exhibit 12 shows the real price movements of four critical agricultural commodities – wheat, rice, corn, and soybeans – in the last few years. Unlike many other commodities, these four are still way below their distant highs, but from their recent lows they have all doubled or tripled.

Bulls will argue that these agricultural commodities are traditional bubbles, based on euphoria and speculation, and are destined to move back to the pre-2002 prices. But ask yourselves what happens when the wheat harvest, for example, comes in. Only the millers and bakers (actually the grain traders who have them as clients) show up to buy. Harvard’s endowment doesn’t offer to take a million tons and store it in Harvard Yard (although my hero, Lord Keynes, is famously said to have once seriously considered stacking two months’ of Britain’s supply in Kings College Chapel!).

The price is set by supply and demand, and storage is limited and expensive. All of the agricultural commodities also interact, so, if one were propped up in price, farmers on the margin would cut back on, say, soybeans and grow more wheat. For all of these commodities to move up together and by so much is way beyond the capabilities of speculators. The bottom line proof is that agricultural reserves are low – dangerously low. There is little room in that fact for there to be any substantial hoarding to exist.

Weather Instability and Price Rises

But there is one factor big enough, on rare occasions, to move all of the agricultural commodities together, and that is weather, particularly droughts and floods. I don’t think the weather instability has ever been as hostile in the last 100 years as it was in the last 12 months. If you were to read a one-paragraph summary of almost any agricultural commodity, you would see weather listed as one of the causes of the price rising.

My sick joke is that Eastern Australia had average rainfall for the last seven years. The first six were the driest six years in the record books, and the seventh was feet deep in unprecedented floods. Such “average” rainfall makes farming difficult. It also makes investing in commodities difficult currently, for the weather this next 12 months is almost certain to be less bad than the last, and perhaps much less bad.

The Unusual Entry Risk Today in Commodity Investing: Weather …

For agricultural commodities, it is generally expected that prices will fall next year if the weather improves. Because global weather last year was, at least for farming, the worst in many decades, this seems like a good bet. The scientific evidence for climate change is, of course, overwhelming. A point of complete agreement among climate scientists is that the most dependable feature of the planet’s warming, other than the relentless increase in the parts per million of CO2 in the atmosphere, is climate instability.

Well, folks, the last 12 months were a monster of instability, and almost all of it bad for farming. Skeptics who have little trouble rationalizing facts will have no trouble at all with weather, which, however dreadful, can never in one single year offer more than a very strong suggestion of long-term change.

Unfortunately, I am confident that we should be resigned to a high probability that extreme weather will be a feature of our collective future. But, if last year was typical, then we really are in for far more serious trouble than anyone expected. More likely, next year will be more accommodating and, quite possibly, just plain friendly. If it is, we will drown, not in rain, but in grain, for everyone is planting every single acre they can till.

And why not? The current prices are either at a record, spent just a few weeks higher in 2008, or were last higher decades ago. The institutional and speculative money does not, in my opinion, drive the spot prices higher for reasons given earlier, but they do persistently move the more distant futures contracts up.

Traditionally, farmers had to bribe speculators to take some of the future price risk off of their hands. Now, Goldman Sachs and others have done such a good job of making the case for commodities as an attractive investment (on the old idea that investors were going to be paid for risk-taking), that the weight of money has pushed up the slope of the curve. This not only destroys the whole reason for investing in futures contracts in the first place, but, critically for this current argument, it lowers the cost to the farmers of laying off their price risk and thus enables, or at least encourages, them to plant more, as they have in spades.

Ironically, institutional investing facilitates larger production and hence lower prices! Should both the sun shine and the rain rain at the right time and place, then we will have an absolutely record crop. This would be wonderful for the sadly reduced reserves, but potentially terrible for the spot price. (Although wheat might be an exception because the largest grower by far – China – is looking to be in very bad shape for its upcoming harvest.)

Today, I will excerpt the part about agriculture, as Grantham's outlook is quite interesting, especially for those of us whose main concern is how to plan smartly for feeding the world during a coming time period of higher priced energy in an oil production constrained world.

My own view is that there is somewhat more resiliency in the Ag/Food system in the near-term, at least, than Grantham expresses, but that depends upon where you live and what our oil price and availability time frame plays out to be.

K. McDonald

_________________________

[...]“The Great Paradigm Shift.”

The primary cause of this change is not just the accelerated size and growth of China, but also its astonishingly high percentage of capital spending, which is over 50% of GDP, a level never before reached by any economy in history, and by a wide margin. Yes, it was aided and abetted by India and most other emerging countries, but still it is remarkable how large a percentage of some commodities China was taking by 2009.

Exhibit 3 shows that among important non-agricultural commodities, China takes a relatively small fraction of the world’s oil, using a little over 10%, which is about in line with its share of GDP (adjusted for purchasing parity). The next lowest is nickel at 36%. The other eight, including cement, coal, and iron ore, rise to around an astonishing 50%! In agricultural commodities, the numbers are more varied and generally lower: 17% of the world’s wheat, 25% of the soybeans (thank Heaven for Brazil!) 28% of the rice, and 46% of the pigs. That’s a lot of pigs!

Source: Barclays Capital 2010, Credit Suisse 2010, Goldman Sachs, United States Geological Survey 2009, BP Statistical Review of World Energy 2009, FAO 2008, IMF 2010

Optimists will answer that the situation that Exhibit 3 describes is at worst temporary, perhaps caused by too many institutions moving into commodities. The Monetary Maniacs may ascribe the entire move to low interest rates. Now, even I know that low rates can have a large effect, at least when combined with moral hazard, on the movement of stocks, but in the short term, there is no real world check on stock prices and they can be, and often are, psychologically flakey. But commodities are made and bought by serious professionals for whom today’s price is life and death. Realistic supply and demand really is the main influence.

[...]

Agricultural Commodities

Moving on to agriculture, the limitations are more hidden. We think of ourselves as having almost unlimited land up our sleeve, but this is misleading because the gap between first-rate and third-rate land can be multiples of output, and only Brazil, and perhaps the Ukraine, have really large potential increments of output. Elsewhere, available land is shrinking. For centuries, cities and towns have tended to be built not on hills or rocky land, but on prime agricultural land in river valleys. This has not helped.

We have, though, had impressive productivity gains per acre in the past, and this has indeed helped a lot. But, sadly, these gains are decreasing. Exhibit 10 shows that at the end of the 1960s, average gains in global productivity stood at 3.5% per year. What an achievement it was to have maintained that kind of increase year after year. It is hardly surprising that the growth in productivity has declined.

It runs now at about one-third of the rate of increase of the 1960s. It is, at 1.25% a year, still an impressive rate, but the trend is clearly slowing while demand has not slowed and, if anything, has been accelerating. And how was this quite massive increase in productivity over the last 50 years maintained? By the even more rapid increase in the use of fertilizer.

Exhibit 11 shows that fertilizer application per acre increased five-fold in the same period that the growth rate of productivity declined. This is a painful relationship, for there is a limit to the usefulness of yet more fertilizer, and as the productivity gains slow to 1%, it bumps into a similar-sized population growth. The increasing use of grain-intensive meat consumption puts further pressure on grain prices as does the regrettable use of corn in ethanol production. (A process that not only deprives us of food, but may not even be energy-positive!) These trends do not suggest much safety margin.

The fertilizer that we used is also part of our extremely finite resources. Potash and potassium are mined and, like all such reserves, the best have gone first. But the most important fertilizer has been nitrogen, and here, unusually, the outlook for the U.S. really is quite good for a few decades because nitrogen is derived mainly from natural gas. This resource is, of course, finite like all of the others, but with recent discoveries, the U.S. in particular is well-placed, especially if in future decades its use for fertilizer is given precedence.

More disturbing by far is the heavy use of oil in all other aspects of agricultural production and distribution. Of all the ways hydrocarbons have allowed us to travel fast in development and to travel beyond our sustainable limits, this is the most disturbing. Rather than our brains, we have used brute energy to boost production.

Water resources both above and below ground are also increasingly scarce and are beginning to bite. Even the subsoil continues to erode. Sooner or later, limitations must be realized and improved techniques such as no-till farming must be dramatically encouraged. We must protect what we have. It really is a crisis that begs for longer-term planning – longer than the typical horizons of corporate earnings or politicians.

The bottom line is, as always, price, and the recent signals are clear. Exhibit 12 shows the real price movements of four critical agricultural commodities – wheat, rice, corn, and soybeans – in the last few years. Unlike many other commodities, these four are still way below their distant highs, but from their recent lows they have all doubled or tripled.

Bulls will argue that these agricultural commodities are traditional bubbles, based on euphoria and speculation, and are destined to move back to the pre-2002 prices. But ask yourselves what happens when the wheat harvest, for example, comes in. Only the millers and bakers (actually the grain traders who have them as clients) show up to buy. Harvard’s endowment doesn’t offer to take a million tons and store it in Harvard Yard (although my hero, Lord Keynes, is famously said to have once seriously considered stacking two months’ of Britain’s supply in Kings College Chapel!).

The price is set by supply and demand, and storage is limited and expensive. All of the agricultural commodities also interact, so, if one were propped up in price, farmers on the margin would cut back on, say, soybeans and grow more wheat. For all of these commodities to move up together and by so much is way beyond the capabilities of speculators. The bottom line proof is that agricultural reserves are low – dangerously low. There is little room in that fact for there to be any substantial hoarding to exist.

Weather Instability and Price Rises

But there is one factor big enough, on rare occasions, to move all of the agricultural commodities together, and that is weather, particularly droughts and floods. I don’t think the weather instability has ever been as hostile in the last 100 years as it was in the last 12 months. If you were to read a one-paragraph summary of almost any agricultural commodity, you would see weather listed as one of the causes of the price rising.

My sick joke is that Eastern Australia had average rainfall for the last seven years. The first six were the driest six years in the record books, and the seventh was feet deep in unprecedented floods. Such “average” rainfall makes farming difficult. It also makes investing in commodities difficult currently, for the weather this next 12 months is almost certain to be less bad than the last, and perhaps much less bad.

The Unusual Entry Risk Today in Commodity Investing: Weather …

For agricultural commodities, it is generally expected that prices will fall next year if the weather improves. Because global weather last year was, at least for farming, the worst in many decades, this seems like a good bet. The scientific evidence for climate change is, of course, overwhelming. A point of complete agreement among climate scientists is that the most dependable feature of the planet’s warming, other than the relentless increase in the parts per million of CO2 in the atmosphere, is climate instability.

Well, folks, the last 12 months were a monster of instability, and almost all of it bad for farming. Skeptics who have little trouble rationalizing facts will have no trouble at all with weather, which, however dreadful, can never in one single year offer more than a very strong suggestion of long-term change.

Unfortunately, I am confident that we should be resigned to a high probability that extreme weather will be a feature of our collective future. But, if last year was typical, then we really are in for far more serious trouble than anyone expected. More likely, next year will be more accommodating and, quite possibly, just plain friendly. If it is, we will drown, not in rain, but in grain, for everyone is planting every single acre they can till.

And why not? The current prices are either at a record, spent just a few weeks higher in 2008, or were last higher decades ago. The institutional and speculative money does not, in my opinion, drive the spot prices higher for reasons given earlier, but they do persistently move the more distant futures contracts up.

Traditionally, farmers had to bribe speculators to take some of the future price risk off of their hands. Now, Goldman Sachs and others have done such a good job of making the case for commodities as an attractive investment (on the old idea that investors were going to be paid for risk-taking), that the weight of money has pushed up the slope of the curve. This not only destroys the whole reason for investing in futures contracts in the first place, but, critically for this current argument, it lowers the cost to the farmers of laying off their price risk and thus enables, or at least encourages, them to plant more, as they have in spades.

Ironically, institutional investing facilitates larger production and hence lower prices! Should both the sun shine and the rain rain at the right time and place, then we will have an absolutely record crop. This would be wonderful for the sadly reduced reserves, but potentially terrible for the spot price. (Although wheat might be an exception because the largest grower by far – China – is looking to be in very bad shape for its upcoming harvest.)

_________________________