photo: usda

The following is a very small excerpt from the latest USDA Vegetable and Melon report. [pdf]

Vegetable and melon production is a diverse, complex, management intensive, and little-subsidized business in the United States. It is also among the more financially successful components of U.S. agriculture. Today, the industry faces an array of challenges:

• Chronic farm labor shortages

• Strong competition in export markets

• Pressure in domestic markets from low-cost imports

• Food safety concerns

• Competition for land and water from both urban encroachment and

alternative crops

• Rising input prices

How the vegetable and melon production industry stands up to these challenges depends in large part on the financial well-being of the backbone of this agricultural sector—the growers.

As measured in a variety of ways, vegetable and melon farms are an important component of U.S. agriculture. U.S. production of vegetables and melons occurs on less than 7 million acres, about 2 percent of all harvested cropland. From this small footprint, however, comes a diverse set of high-value products, which generated 14 percent of all farm crop cash receipts and 6 percent of U.S. farm export value during 2005-07 (USDA, ERS(g)). U.S. per capita consumption of all fresh and processing vegetables averaged 435 pounds during 2005-07, down slightly from 1995-97 but 12 percent above 1985-87.

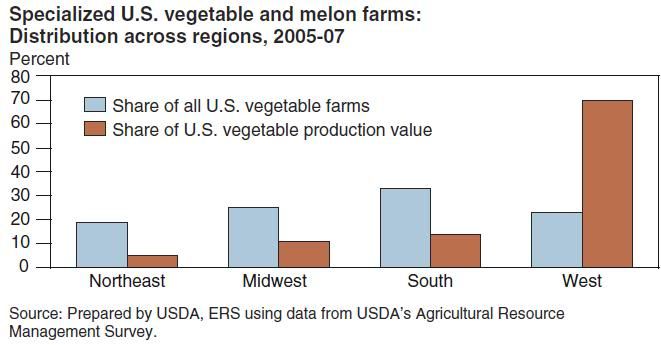

According to data derived from ARMS, these specialized farms represent the bulk of U.S. vegetable and melon output, relying heavily on vegetable sales for a substantial proportion of their farm income. On average, specialized vegetable farms accounted for 55 percent of all the farms producing vegetables in the United States and contributed 88 percent of the total value of U.S. vegetable production during 2005-07. The remainder of product sales on these farms came from such commodities as cotton or grain. Regionally, these farms tend to be most heavily concentrated in the South, with substantial numbers also found in the Midwest and West. However, the West dominates in terms of vegetable crop value, with about two-thirds of the U.S. total for vegetable and melon farms in 2005-07. Although a significant volume of vegetables is also grown in the Midwest and Northeast, operations in these areas tend to rely more on other crops for their farm revenue.

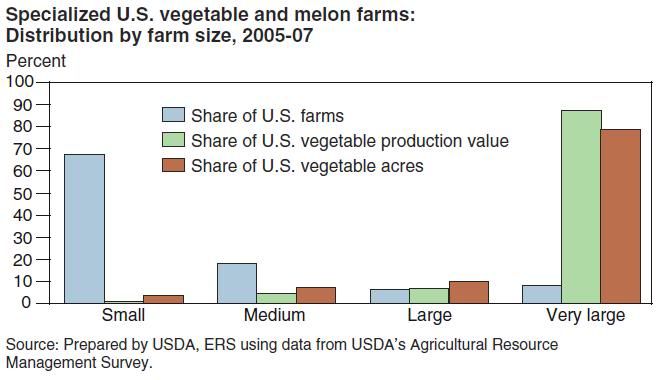

About 8 percent of all specialized vegetable and melon farms produced $1 million or more of agricultural commodities per year during 2005-07. These large commercial farms accounted for 87 percent of the total value of U.S. vegetable production. Given the relatively high per acre values of such crops as potatoes, tomatoes, peppers, and asparagus, harvested area of these commodities is highly concentrated among farms with more than $1 million in sales per year. For example, data from the 2007 Census of Agriculture show that 93 percent of the area for tomatoes grown for processing and 83 percent of the area for all potatoes come from farms with $1 million or more in sales. Potatoes and tomatoes are the two single largest U.S. vegetable crops in terms of production and per capita use. Combined, these two crops account for about one-fourth of all vegetable and melon cash receipts.

The very large farms accounted for 87 percent of the total value of vegetables produced by all specialized vegetable farms and tend to be concentrated in the West. Vegetable and melon farms that produced less than $40,000 worth of commodities (small farms) per year made up 67 percent of these farms yet accounted for just 1 percent of the total value of U.S. vegetable production. Small farms are largely concentrated in the South. As with most agricultural commodities, vegetable production has become increasingly concentrated over time as larger, more efficient farms have garnered a greater share of the domestic market.