photo source

While everyone knows that most agricultural subsidies in the U.S. go towards the production of grains, this report focuses on the production data of vegetables, melons, sweet corn, potatoes, dry beans, and other good dietary food for human consumption. That fact alone makes this report important, in my opinion.

These are some of the same foods that are being produced in the urban agriculture movement and the growing vibrant farmer's markets and CSA's popping up across this nation. Since I saw no reference to how these strong movements are affecting commercial production of these staples, I contacted the USDA authors and they confirmed that this study only looks at commercial growers.

As the efficiencies of industrial ag's grain production are slowly removed from the status quo policy of over-production by way of higher energy induced input costs, it seems likely that this sector will gain greater agricultural importance over time. By some estimates we should be devoting 13 million more acres of farmland to growing fruits and vegetables just for Americans to meet the minimum daily requirements.

To follow, are snippets which I found most interesting from the recent USDA report, the first being a good example of the law of supply and demand as dry bean prices were high in '09 which produced a surplus of supply this year:

- With generally favorable harvest weather, national production of all dry beans is estimated at 32.6 million cwt, up 29 percent from the relatively modest crop of a ear earlier. Output has equaled or exceeded 30 million cwt in just 8 of the past 100 years. National yield is estimated to be a record 17.83 bags (cwt) per acre—up 3 percent from a year earlier and 1 percent above the previous high set in 2008. Based on acreage and projected yields by class, output is expected to rise for at least 8 bean classes including pinto, navy, Great Northern, black, garbanzo, pink, and dark red kidney. Lentil harvest area is expected up 56 percent to 639,000 acres, while dry pea area is estimated to be up slightly to 842,900 acres. With possible strong yields, production could be higher than last year’s records.

- With a combination of slightly lower area and reduced yields, production of fall storage onions is expected to decline 5 percent from a year earlier to 54.7 million cwt. As a result of the smaller fresh-market storage crop and continued good domestic and export demand, onion prices may remain above year-earlier levels until next spring.

- The 2010 U.S. processing tomato crop will likely total about 12.8 million tons—well under last year’s total but will be the second or third highest on record. With weather limiting output in some competing nations, lower U.S. wholesale prices, and the weak dollar helping to make U.S. prices even more competitive in the world, exports of tomato products are expected to rise during the coming marketing season.

- Retail prices for fresh-market vegetables averaged 3 percent above a year earlier during the summer quarter (July-September) of 2010. With the exception of crops such as asparagus, sweet corn, cabbage, and romaine lettuce, average retail prices were higher for most all major vegetables.

- Although wholesale prices for melons averaged above a year earlier this past summer, retail prices were lower.

- During the summer quarter of 2010, retail prices for processed fruits and vegetables averaged 1 percent below a year earlier but 3 percent higher than 2 years earlier. Compared with last summer, consumers paid 2 percent less for frozen vegetables and 1 percent less for canned vegetables. Canned vegetable prices remain 6 percent above 2 years earlier despite sharply lower contract prices for raw vegetables this year.

- Although the volume of fresh-market potato exports was up 15 percent from

2008/09, the average export unit value (price) was down 20 percent, leaving the

value of fresh exports 8 percent lower than a year earlier. - During the summer of 2010, wholesale prices for U.S. freshmarket sweet potatoes averaged 8 percent above a year earlier due to strong demand for fresh and processed use. Advertised retail prices for sweet potatoes averaged $0.97 per pound this summer—also up 8 percent from a year earlier.

- With prospects for improved supplies and weaker grower and dealer prices for many bean classes, retail prices for dry packaged edible beans averaged $1.31 per pound this summer, down 6 percent from a year earlier.

- With larger supplies in 2009 and 2010, grower prices for dry edible peas averaged 15 percent below the highs of a year earlier during July-September. Similarly, grower prices for lentils averaged 18 percent below a year earlier during the same time period.

- Production of all asparagus (fresh and processing) continued to recede in 2010, falling 18 percent to 0.74 million cwt—the smallest asparagus crop on record. A combination of lower harvested area (down 4 percent) and reduced yield (down 16 percent) accounted for most of the decline. Production used in the fresh-market dropped 12 percent, while crop destined for processing plummeted 39 percent to just 6,000 tons (about evenly split between canning and freezing use). Growers have reduced asparagus area 65 percent over the last decade, largely in response to increased import competition. U.S. asparagus imports largely come from two countries, Peru and Mexico.

U.S. EXPORTS:

- Canada was up 8 percent from a year earlier led by head lettuce and bulb onions

- Mexico was up 34 percent led by tomatoes and bulb onions

- Japan, up 38 percent led by broccoli and asparagus

- Taiwan, up 21 percent led by broccoli and head lettuce

- United Kingdom, up 20 percent led by sweet potatoes and sweet corn

- Together, Canada and Japan accounted for 84 percent of U.S. fresh-market vegetable export volume during the first 8 months of 2010—an increase in concentration among the top two markets from 77 percent a decade earlier.

- Raw tomatoes (including fees) account for about half of the cost of a pound of tomato paste, the basic ingredient in many processed tomato products (e.g., catsup, sauces, and juice).

U.S. IMPORTS:

- Through August, the top five sources of processed vegetable imports this year include Mexico (27 percent of the total), China (14 percent), Canada (11 percent), Peru (7 percent), and India (5 percent).

- Prospects for the world supply situation of potatoes in 2010/11 continue to look tight.

- With a surge in volume of black beans, mung beans, and a wide variety of other beans, China took over the top spot as the number one exporter of dry beans to the United States.

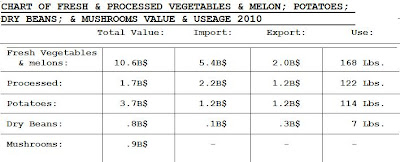

OVERALL STATISTICS:

- Fresh vegetable and melon total value: 10.6 B$ 2010; processed 1.7B; potatoes 3.7; .8 dry beans; .9 mushrooms

- We imported: vegetables and melons 5.4B$; processed 2.2B$; potatoes 1.2B$

- We exported: vegetables and melons 2.0B$; processed 1.2B$; potatoes 1.2B$

- Per capita use of fresh vegetables and melons: 168 lbs; processed 122 lbs; potatoes and products 114 lbs; dry beans 7 lbs.

- Per capita net domestic disappearance of potatoes for calendar year 2009 totaled 113.1 pounds (fresh-weight basis), down 4 percent from 2008. The decline in the domestic use of potatoes can be attributed to the impact of recession on demand (particularly in foodservice), a small 2008 crop (which limited domestic shipments from storage), quality problems with the 2009 fall crop, and continued high exports. Per capita disappearance of all potatoes was the lowest since 1980.

---Kalpa

source: usda [pdf]