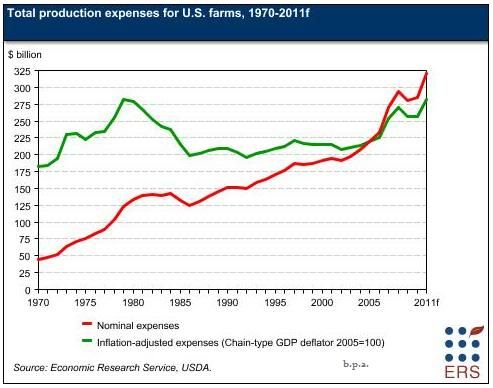

Production Expenses Rise More Than $30 Billion in 2011

After falling $12.0 billion (4.1 percent) in 2009 and rebounding a relatively modest $4.5 billion (1.6 percent) in 2010, total production expenses are set to rise $34.4 billion (12.0 percent) in 2011 to a nominal record $320.0 billion. The 2011 jump resembles the large increases in production expenses in 2007 and 2008. This is the first time that expenses will have exceeded $300 billion. When adjusted for inflation, 2011 expenses also set a record, surpassing the previous peak reached in 1979.

On the price side, total expenses are affected by an expected 12-percent increase in the Production Items, Interest, Taxes, and Wage Rate (PITW) prices-paid index. On the quantity side, total output (and therefore the quantity of inputs used) is predicted to decrease by 4.4 percent for crops and increase 1.1 percent for livestock. As a result, total output will be down 2.3 percent. Planted acres are forecast up 0.2 percent.

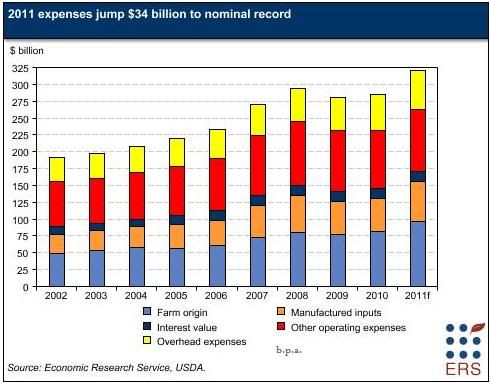

Every expense except labor and electricity is forecast to increase in 2011. Feed is expected to rise $10.3 billion (23 percent); livestock and poultry purchases, $3.5 billion (18 percent); fertilizer and lime, $5.8 billion (28 percent); and fuels and oils, $3.5 billion (27 percent). Seeds, miscellaneous expenses, repair and maintenance, and net rent to nonoperators should each be up more than $1 billion in 2011.

The increase in expenses will affect crop and livestock farms differently.

The principal expenses for livestock farms are expected to increase nearly $13.8 billion (18.5 percent), while the principal crop expenses are expected to increase $7.0 billion (14.7 percent).

In addition, the value of crop production is expected to rise 18.5 percent while the value of livestock production is forecast to go up 16.6 percent, so the increase in expenses will impinge on net incomes of livestock farms more than crop farms.

After rising $18.9 billion (67 percent) from 2006 to 2008, feed expenses fell almost $2 billion in 2009 and were up less than 1 percent in 2010.

In 2011, feed expenses are forecast to rise by $10.3 billion (23 percent).

Two factors contributing to this forecast are a 21-percent increase in the feed prices-paid index and the 1-percent projected rise in livestock output. The rise in the feed prices is due primarily to the forecast jump in feed grain and oilseed prices. The calendar-year price for corn, which constitutes over 90 percent of feed grains used, is expected to increase 57 percent in 2011.

The calendar-year price for soybeans—the primary ingredient in soymeal, the principal oilseed feedstock—is expected to be up around 27 percent. The increase in feed prices will not be as great as the increase in underlying commodity prices because price changes for complete feeds, which have the heaviest weight in the prices-paid index, lag price changes in raw inputs used to manufacture complete feeds.

The feed and residual use of feed grains should be down around 3 percent in 2011. Again, this drop may not be reflected in the amount of complete feeds fed because of the lag between the input of raw materials and the finished product. Also, the demand for feed from feedlots will be heavier than the net placements of cattle-on-feed suggests. Lighter feeder cattle are being sent to feedlots because of poor pasture conditions in some areas. These cattle will consume more feed while in the feedlot. Additionally, the number of grain-consuming animal units should rise around 1 percent in 2011.

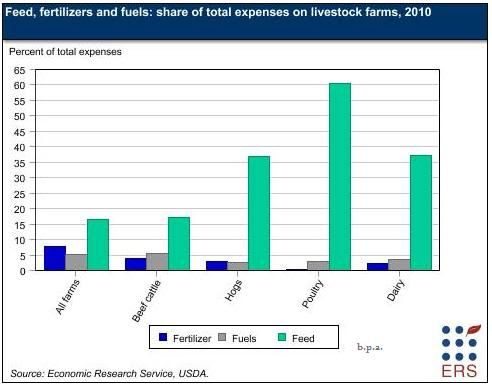

Livestock and poultry purchases are forecast to be up $3.5 billion (18.0 percent) in 2011. Since cattle account for 75 percent of this expense, conditions in the cattle market are the main driver of these purchases. Net placements of cattle-on-feed for 2011 are forecast to be nearly the same as in 2010, but the cost of feeder cattle should be up over 16 percent because of abnormally tight inventories, stable demand for beef products, high prices for Choice retail beef, and brisk exports. High retail prices for all beef products allowed feedlot operators to earn favorable returns for a time despite higher feeder cattle and feed costs.

According to ERS' High Plains Cattle Feeding Simulator, the net margin in feedlots was positive between October 2010 and April 2011. Returns have gone negative since April, however, as feed and feeder costs have risen faster than the price for fed cattle. With respect to other animals, pork production should be up 1 percent in 2011 and prices for hog feeders are forecast to increase 17 percent. Broiler production is forecast down slightly, while prices should be up a small amount.

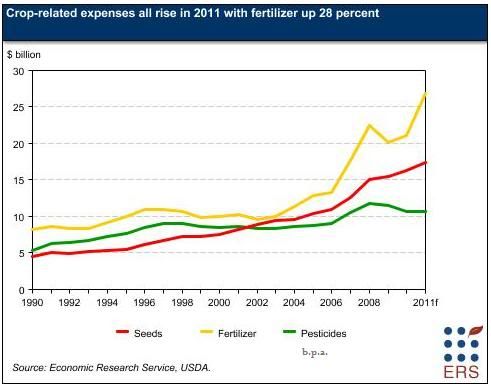

The principal crop-related expenses grew 77 percent between 2002 and 2008, with 48 percent of the rise occurring in 2007-08. During 2009-10, the climb stalled; crop-related expenses fell 4.5 percent in 2009 and recovered only 1.7 percent in 2010. The primary reason for this pattern was movements in fertilizer expenses, which jumped 134 percent during 2002-08 and then dropped 11 percent in 2009 before rising 4.5 percent in 2010.

Crop-related expenses are expected to rise 14.7 percent in 2011, again due largely to an expected increase of almost 28 percent in fertilizer expenses.

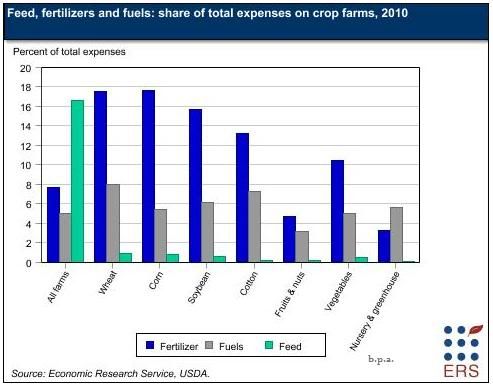

The principal driver of crop-related expenses throughout 2002-2011 has been changing input prices. Acres planted to principal crops have not been a factor in the long-term growth in these expenses since they have never exceeded the 327 million acres planted in 2002. Use of pesticides and more expensive seeds with increasingly complex genetic traits has increased, and this demand has been a factor in rising prices over this period. Increases in the price of natural gas, a principal source of many fertilizers, have contributed to the rise in fertilizer prices. The average annual price for natural gas was $2.95 per thousand cubic feet (tcf) in 2002. Its price in 2008, the year that the fertilizer prices-paid index reached its highest level, was $7.96 per tcf.

Prices for all crop-related inputs are expected to be up in 2011. Acres planted to principal crops will not be a big factor this year, as they are forecast to rise only 0.2 percent. Overall, grain and oilseed production should be down almost 6 percent. However, acres planted to corn, a heavy user of inputs, are forecast to have expanded 3.7 million acres in 2011. Production of fruits, nuts, and vegetables should be nearly the same as in 2010, and cotton production is forecast down 10 percent.

Between 1999 and 2008, prices paid for seeds rose 146 percent, with 64 percent of that rise occurring during 2006-09, and seed expenses increased $8.3 billion (115 percent). During the 2006-08 period alone, seed expenses jumped $4.1 billion (37 percent).

The upward movement in seed costs slowed considerably in 2009 and 2010, with seed expenses rising only 8 percent. In 2011, seed purchases are predicted to rise almost $1.1 billion (6.7 percent) because of a rise of 6.5 percent in prices paid for seeds and the slight expansion in acres planted.

Fertilizer prices rose steadily between 2002 and 2008, with the annual average prices paid for fertilizers climbing 264 percent. During this period, fertilizer expenses rose $12.9 billion (134 percent).

These increases abruptly halted in 2009, when fertilizer expenses dropped $2.4 billion (11 percent). As with seeds, fertilizer expenses rose around 5 percent in 2010. In 2011, fertilizer expenses are forecast to resume their steep climb, going up $5.8 billion (28 percent), as annual average prices paid rise nearly that much. One factor in this increase will be higher demand due to the increase in corn planted acreage. Also, the cost of oil, which influences the cost of many fertilizers, will likely continue to go up throughout 2011.

Pesticide expenses also rose steadily from 2002 to 2008. In 2007 and 2008 alone, they rose $2.7 billion (30 percent).

Since prices paid for pesticides rose only 8.4 percent during those 2 years, increased use was the major reason for increases in this expense. Even though prices paid for pesticides continued to increase in 2009, pesticide expenditures fell slightly. Another decrease of about 8 percent ($900 million) occurred in 2010 as prices paid for pesticides fell and planted acreage declined. During 2009 and 2010, pesticide expenses fell more than 9 percent. In 2011, pesticide expenses are forecast to rise around $100 million (1.0 percent) as a result of a 1-percent rise in prices paid and a slight increase in planted acres.

As with fertilizer, prices paid for fuel rose dramatically between 2002 and 2008. During this period, annual average prices paid for fuel jumped 207 percent, registering 6 straight double-digit percentage increases, and fuel and oil expenses shot up $9.6 billion (146 percent).

Prices paid for fuels then fell 34 percent in 2009 and expenditures dipped $3.5 billion (22 percent). Annual average prices paid for fuels were back up in 2010 and expenditures rose almost $500 million (4 percent). In 2011, prices paid are forecast to rise another 27 percent as Refiner Acquisition Cost (RAC) is expected to increase 32 percent. The price movement and increased acreage are forecast to raise expenditures for fuels and oils by $3.5 billion (27.0 percent).

source