photo: flickr

Note that this post is taken from a report by Jason Henderson and Brian Briggeman for the Federal Reserve Bank of Kansas City, "What are the Risks in Today’s Farmland Market?"

Capitalizing Future Revenues

If historical relationships hold true, Midwestern cropland values hinge on farm revenues, interest rates and their relationship with the capitalization rate. Assuming average Midwestern crop yields, various combinations of corn prices and capitalization rates can rationalize current cropland values. However, all of these combinations assume historically high crop prices or historically low capitalization rates, which raise the risk in land markets.

With economic models suggesting that today’s historically high farm revenues have been capitalized at historically low rates of return, agricultural real estate values could fall sharply if crop prices sag or future interest rates rise.

To illustrate the risk facing farmland values, a straight forward net present value model is used to determine the capitalized value of future crop revenues (Lamb and Henderson). Assuming constant revenues in the future and a constant capitalization rate, cropland values can be determined by:

Cropland values = Future revenues ÷ Capitalization rate. (1)

In this model, future revenues are limited to the returns that are reinvested into the land or the amount received by the landowner. While the returns to land vary with farm profitability, the portion of gross revenues allocated to land owners has remained fairly constant over time. Over the past three decades, USDA costs of production data indicate that land owners receive about 25 percent of all gross revenues generated from cropland.

Therefore, future revenues can be estimated as a quarter of expected farm revenues, based on expected crop prices and yields. As discussed earlier, capitalization rates can be proxied with historical cash rent-to land value ratios.

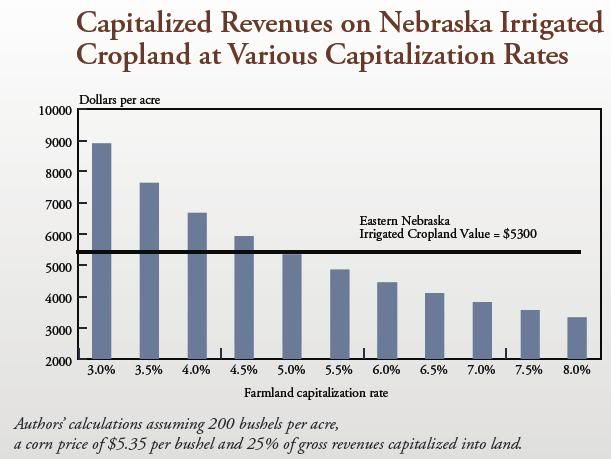

Using equation (1), current farmland values appear to reflect current market conditions. For example, the current average market price for irrigated cropland in eastern Nebraska is estimated to be roughly $5,300 per acre. Assuming an average corn yield of 200 bushels per acre, an average 2010 farm-level corn price of $5.35 per bushel and Nebraska’s average 2010 capitalization rate of 5.1 percent, the capitalized cropland value is estimated at roughly $5,300 per acre ($5.35 *200 *0.25 ÷ 0.051 = $5,245).

Analyses of farmland values in other regions of the nation produced similar results, also suggesting that current farmland values reflect high farm revenues and low capitalization rates. Nevertheless, farmland values face significant risk. If returns on alternative investments rebound, capitalization rates could increase and cut farmland values. For example, with prices remaining constant and capitalization rates rising to their historical average of 7.5 percent, eastern Nebraska’s irrigated cropland values could drop by almost a third (Chart below).

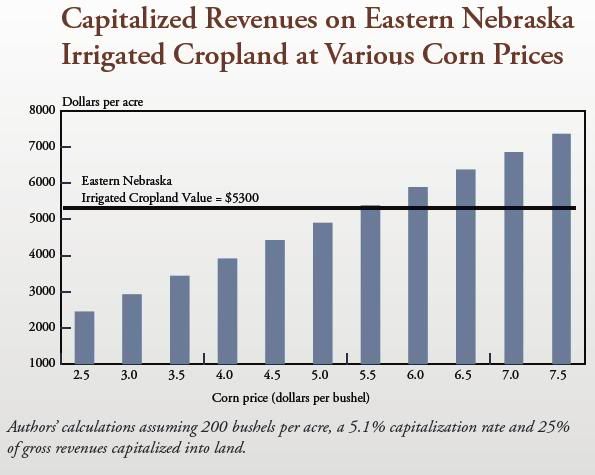

Farmland values could also fall if farm revenues decline. In response to today’s current high commodity prices, U.S. farmers are expected to expand their crop production. With larger production, crop inventories are projected to rise, placing downward pressure on crop prices. In fact, by 2013, USDA projects U.S. corn prices to fall to $4.10 per bushel with larger inventories. If these expectations are realized and corn prices fall to $4 per bushel, irrigated cropland values in eastern Nebraska could fall more than 20 percent, even if capitalization rates remain at today’s historically low levels (Chart below).

The worst-case scenario is a combination of higher capitalization rates and falling farm revenues. In 1981, the spike in real interest rates pushed capitalization rates to historic highs. At the same time, high interest rates contributed to higher exchange rates, lower agricultural exports, falling commodity prices, and cuts in farm revenues. From 1981 to 1987, the combination of higher capitalization rates and falling revenues contributed to a 40 percent decline in real U.S. farmland values, with even larger declines in nominal farmland values.

If similar events occur in today’s environment, farmland values could plummet. For example, in eastern Nebraska, if capitalization rates return to their historic average of 7.5 percent and corn prices fall to $4 per bushel, then irrigated cropland values could fall nearly 50 percent to about $2,600 per acre. Other regions face similar risks.

Summary

Farmland values soared at the end of 2010. Strong demand and tight supplies fueled a spike in U.S. crop prices, while low interest rates contributed to both lower capitalization rates and higher commodity prices. Across much of the Midwest, rising farmland values have outstripped the increases in cash rents, raising questions about the sustainability of current values. In the long-term, future farm revenue expectations and interest rates should determine farmland values. Today, the interest rate risk to farmland values is high. Record high farmland values are based on expectations of interest rates remaining low for an extended period. As the economy strengthens, however, interest rates could rise, which may lift capitalization rates and lower farm revenues. Events such as these could become a recipe for falling land values and the erosion of farm wealth.

source