photo: flickr

Note: The following is from the USDA's outlook report on Vegetables and melons... Dry beans are another food which is becoming more expensive due to the corn ethanol program. This food is an excellent healthy source of protein and contributes to our nation's food security. Not mentioned in the report is that dry beans are a more affordable protein and given the current recession, increased disappearance might also be attributed to grocery consumer weakness.

K. McDonald

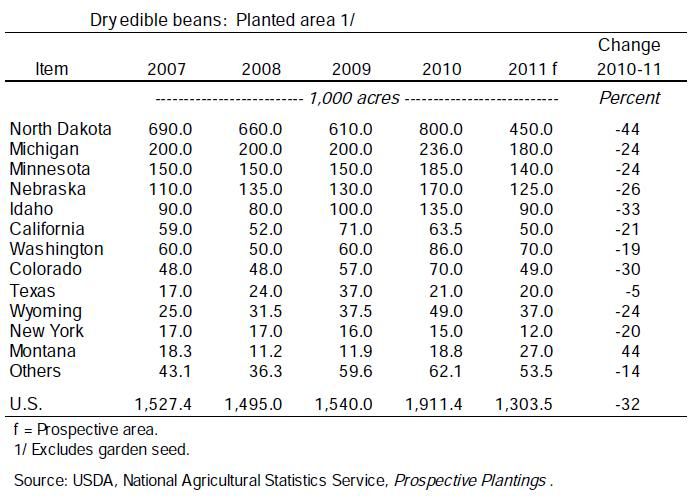

Prospective dry bean area is down 32 percent due to carryover from last year’s large crop and strong returns for competing crops such as corn, soybeans, and wheat. As a result, grower prices are averaging above a year earlier for nearly every reported bean type.

With prices for competing crops generally higher than a year earlier, growers intend to plant less area to dry peas, Austrian winter peas, and chickpeas. However, the revenue incentive for lentils remains strong; if realized, planted area could reach a record high.

Dry edible beans: Given strong supplies from last fall’s large crop, per capita disappearance of dry beans rose 19 percent in 2010 to 7.2 pounds—led by increased use of pinto, navy, and garbanzo beans. With a much smaller crop and higher prices expected in 2011, net domestic use of dry edible beans is expected to decline.

Dry peas and lentils: Per capita disappearance of dry peas (excluding chickpeas) and lentils for domestic human food was estimated at 1.2 pounds, up 20 percent from a year earlier. In the year ahead, domestic use of lentils will likely rise but lower dry pea use will pull use of all dry peas and lentils below 2010 levels.

~~~~~~~~~~~

Prospective Area Drops 32 Percent

As expected, dry bean growers have indicated they plan to reduce area planted to the various bean classes 32 percent from last year’s high level. According to USDA’s Prospective Plantings, area planted to dry edible beans is expected to decline 32 percent this spring from last year’s 1.91 million acres. If realized, this would be the smallest dry bean seeded area since 1983. Final planted area depends on factors such as weather (e.g., excess spring rain may favor increased dry bean area since beans have a shorter growing season) and changes in relative price relationships among crops. This year, prospective dry bean area was down due to carryover from last year’s large crop and also because of the broad price strength exhibited among competing crops, especially corn, soybeans, and wheat.

Dry bean area is under pressure in North Dakota (the largest dry bean producer) with acreage gains projected for crops such as corn, soybeans (a record high), wheat, and sugarbeets. This is also where an increase from intended dry bean area is likely since projected dry bean area in North Dakota was very low, the State is the industry leader in dry beans, and is also the top producer of pinto and navy beans. In fact, grower prices for pinto beans increased shortly after the intentions report was released in a likely bid to gain more pinto bean area.

With the exception of Montana (which plants mostly pinto and garbanzo) and South Dakota, dry bean acreage was expected to decline in all 18 surveyed States. Both of these States are relatively minor dry bean suppliers. Although Montana’s dry bean area was projected to reach 27,000 acres, it would be the largest area since 2001.

In South Dakota, which primarily produces pinto, garbanzo, and navy beans, the prospective dry bean area would be the highest since 2006. Since planting does not finish until June in some areas, further adjustments to indicated acreage will likely take place. The next acreage estimate for dry beans will be released in the June 30 Acreage report.

Assuming planted area remains near 1.3 million acres and 4 percent of acreage is unharvested (the average loss during 2008-10), harvested area would be around 1.25 million acres. This would be down 32 percent and similar to area harvested in 2001 but above the recent low reached in 2004 when untimely rain and frost caused low yields and 10 percent of area to be lost.

If yields reach the average of the past 3 years (17.4 hundredweight (cwt)), 2011 yield would be higher than either of the past 2 years. The 50-year trend yield would be nearly the same as the 3-year average. As a result, dry bean production would decline to about 22 million cwt—the smallest crop since 2004. As a result, stocks will be drawn down and prices will likely remain under pressure relative to historical levels in order to maintain revenue parity with other field crops and preserve grower interest in dry beans.

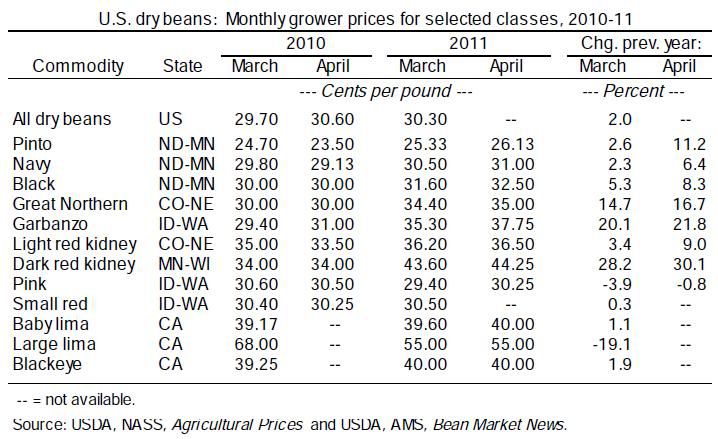

Prices Above a Year Earlier

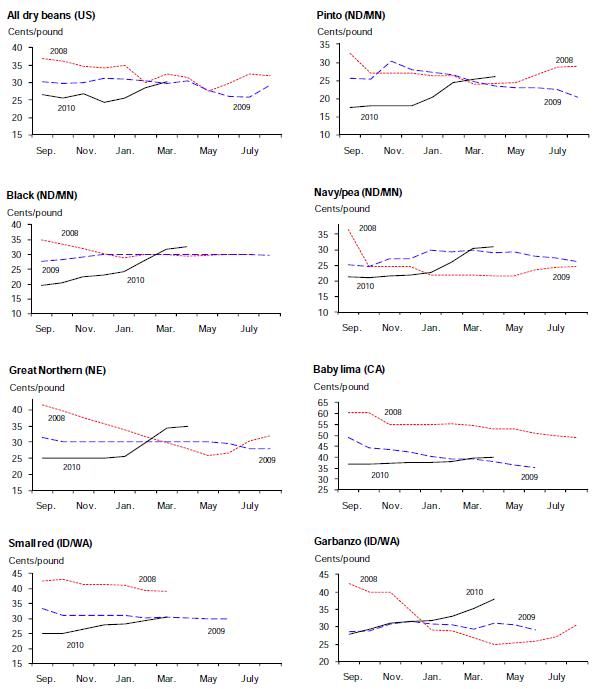

In April, with the exception of large limas and pink beans, grower prices are averaging above a year earlier for every reported class of dry bean. With the exception of pinto beans, grower bids are at least $30 for every dry bean class. Partly because dry bean production for individual classes tends to be regionalized, prices largely react to their own set of supply and demand characteristics. However, like the situation in 2007-08, the external pressure generated by high returns for most other field crops has affected dry bean markets and caused prices to push higher.

For example, April pinto bean prices in the upper Midwest averaged $26.13 per cwt—11 percent above the previous year despite the presence of large stocks from last fall’s crop. Dark red kidney beans in Minnesota/Wisconsin averaged $44.25 per cwt this April—up 30 percent from a year earlier. The preliminary 2010/11 season-average grower price for all dry beans was estimated at $26 per hundredweight (cwt)—down 13 percent from a year earlier but 12 percent above the average of the previous decade (2000-09). It was also the fourth highest season-average dry bean price (unadjusted for inflation) over the past 20 years.

Dry bean prices continue to creep upward this spring as a result of both basic supply-and-demand forces within the dry bean complex plus upward pressure from crop markets competing for limited acreage. In 2011/12, the season-average price is expected to exceed $32/cwt and could remain over $30 in 2012/13.

Per Capita Disappearance Rises

Disappearance (net domestic use, a proxy for consumption) of dry edible beans increased in 2010 (calendar-year estimate). With greater domestic availability (due mostly to a sizeable increase in the 2010 crop) and lower prices, domestic use rose to 2.2 billion pounds. When expressed on a per person basis, net domestic use of dry beans increased 19 percent to 7.2 pounds—up 1.2 pounds from the low of 6.03 pounds reached in 2009. In 2011, domestic dry bean use is expected to decline due to the expected smaller crop, continued good export demand, and higher dry bean prices, which will offset higher carryin stocks from 2010.

Excluding garbanzo beans, which are sometimes grouped with dry peas and lentils, per capita use of dry beans is forecast to total 6.2 pounds in 2011, down 8 percent from a year earlier. In 2010, gains in per capita net domestic use were noted for both white (up 26 percent) and nonwhite (up 17 percent) bean types. White beans (navy, Great Northern, lima, and small white) accounted for 17 percent of all dry beans available domestically, similar to a year earlier but down from 24 percent a decade ago.

White bean disappearance increased for all classes but large lima. Most of the gain came from navy beans, which resulted from a 43-percent increase in production. With per capita disappearance rising to 5.9 pounds in 2010, nonwhite beans (e.g., pinto, dark red kidney, black, etc.) remained dominant, led by pinto beans, black beans, and the surging popularity of garbanzo beans (mostly kabuli chickpeas).

Driven by two consecutive strong crops in 2009 and 2010, domestic disappearance of black beans was second only to the 1999 record high. Garbanzo bean use was also strong in 2010, with disappearance second only to the 2007 record high. Over the past 3 years (2008-10), per capita use of garbanzo beans averaged 0.39 pounds—up 58 percent from a decade earlier (1998-2000). Rising use likely reflects the increased popularity of vegan/vegetarian foods, Middle Eastern cuisines, and Indian/Indian subcontinent cuisines.

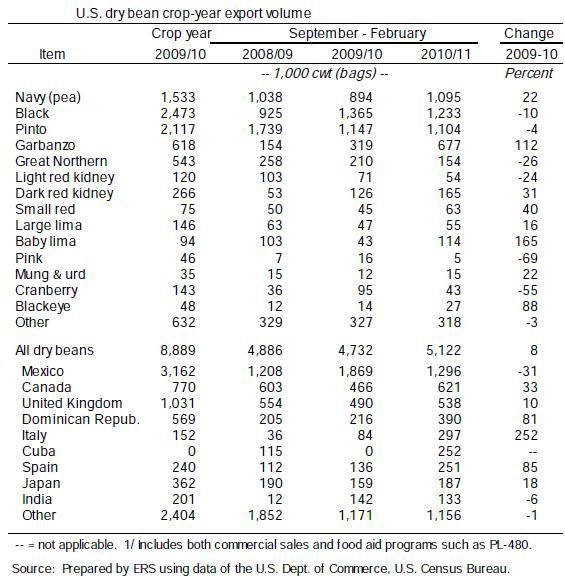

Export Volume Up 8 Percent

During the first 6 months of the marketing year (September 2010-February 2011), U.S. exports of dry beans increased 8 percent from a year earlier to 5.1 million bags (cwt). This was the largest 6-month export volume since the 1994/95 season. Among the fourteen identified export classes, eight exhibited export gains including baby limas (up 165 percent), garbanzos (up 112 percent), and navy beans (up 22 percent).

Exports of black beans, the top export class in 2009/10, were down 10 percent through February as demand from Mexico has declined (table 20). Although average export value is slightly higher this year, export volume has remained resilient despite a 31-percent reduction in shipments to Mexico, the top destination. Movement into Mexico was lower for black, pinto and navy beans. At the same time, U.S. dry bean exports to Canada, the second largest market, jumped 33 percent on the strength of increased movement of navy beans and garbanzo beans.

Exports to the United Kingdom were up 10 percent due to greater navy bean, garbanzo bean, and black bean shipments. Exports to Italy and Spain each showed strong gains due mostly to greater demand for navy beans, garbanzo beans, and dark red kidney beans. Volume shipped to the Dominican Republic increased due mostly to movement of pinto beans. For all dry beans, the September-February 2010/11 average U.S. dry bean export unit value was up just 1 percent from the previous year to 33.4 cents per pound.

Grower bids for U.S. dry edible beans, 2008/09-10/11:

Source: USDA, Agricultural Marketing Service, Bean Market News.

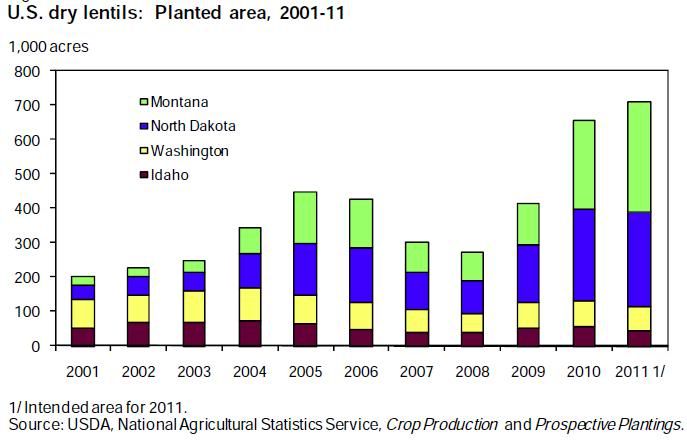

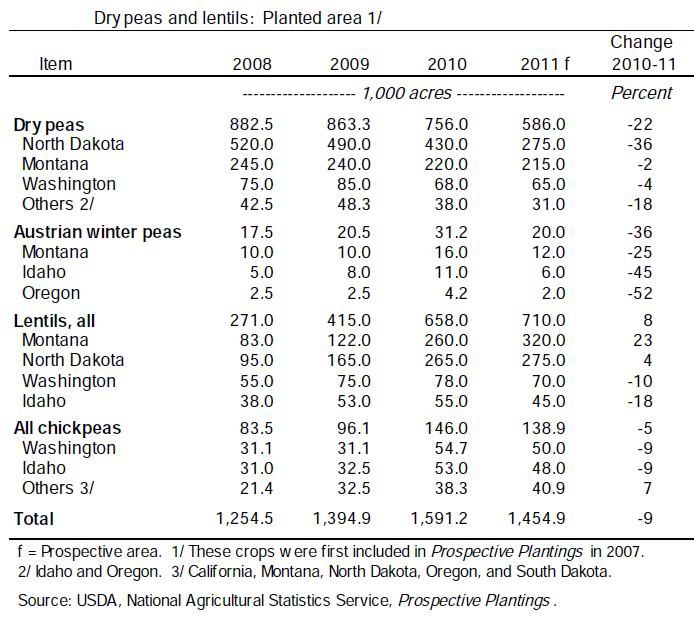

Lentil Area Continues To Expand, Dry Peas Decline

According to the USDA’s Prospective Plantings, aggregate area planted to dry peas, Austrian winter peas, chickpeas, and lentils is expected to drop 9 percent this spring from last year’s 1.59 million acres. With prices for competing crops generally higher than a year earlier, growers intend to plant less area to dry peas, Austrian winter peas, and large chickpeas. However, the revenue incentive for lentils remains strong; if realized, planted area could reach a record high.

For lentils, all the gain in intended area is in Montana and North Dakota with declines reported for Idaho and Washington. In Canada, lentil growers are expected to drop planted area by 22 percent in response to a large carryover of low-quality lentils, which has suppressed 2010/11 prices and will likely dampen 2011/12 returns compared with other crops. U.S. dry pea growers intend to plant less area for the third consecutive year; if realized, planted area would be the lowest since 2004.

Declines are expected in Washington, Idaho, and Oregon—where the majority of top-grade food peas are produced—and in North Dakota and Montana—where the majority of yellow and green feed peas are produced. Canadian dry edible pea planted area (down 7 percent) and output are also expected lower this year. Although overall U.S. chickpea area is expected to decline, growers in Montana intend to almost treble planted area to 18,000 acres, levels not seen since the early 2000s. Canadian planted area is expected to rise 2 percent as growers anticipate strong chickpea revenues compared with many other crops.

Export Volume Down, Imports Up

U.S. export volume (including food aid) of all dry peas and lentils (excluding seed) totaled 11.3 million cwt over the first 8 months (July-February) of the 2010/11 marketing year, an 11-percent decline from a year earlier. India (28 percent of total volume) and Canada (8 percent) remained the top destinations. Although down 35 percent from the high levels of July-February 2009/10, India’s imports of U.S. dry peas and lentils were more than double the quantity shipped during the same period in 2008/09. Spain accounted for one third of the increase in chickpeas exports. Because of quality problems with the Canadian lentil crop, year-to-date exports of lentils to Canada surged to 410,191 cwt, up from 76,898 cwt a year earlier.

source