photo source: usda

- Cotton is one of the most important textile fibers in the world, accounting for around 35 percent of total world fiber use.

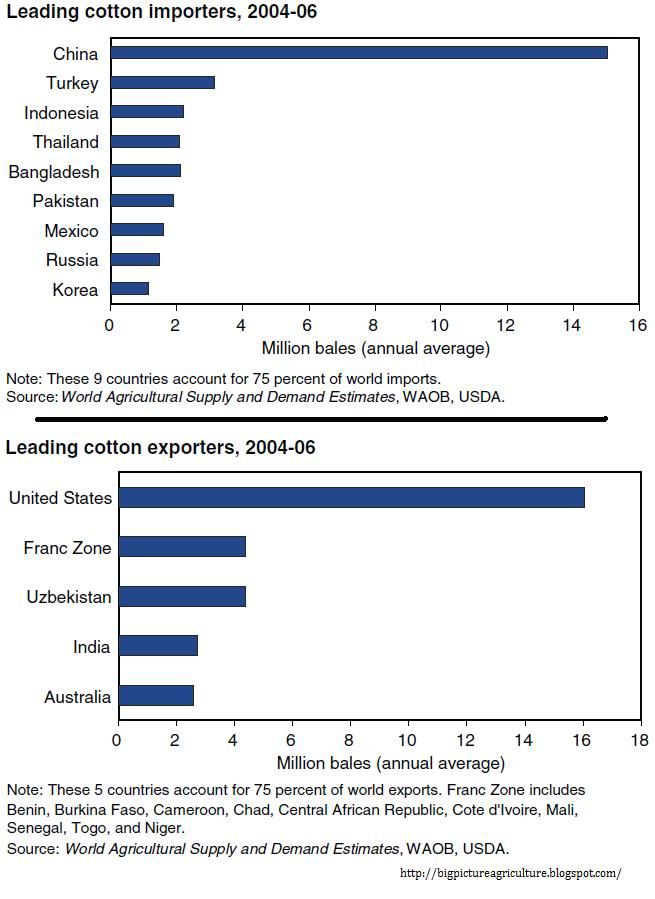

- While some 80 countries from around the globe produce cotton, the United States, China, and India together provide two-thirds of the world's cotton.

- The United States, which ranks third in production behind China and India, is the leading exporter, accounting for over one-third of global trade in raw cotton.

- The U.S. cotton industry accounts for more than $25 billion in products and services annually, generating about 200,000 jobs in the industry sectors from farm to textile mill.

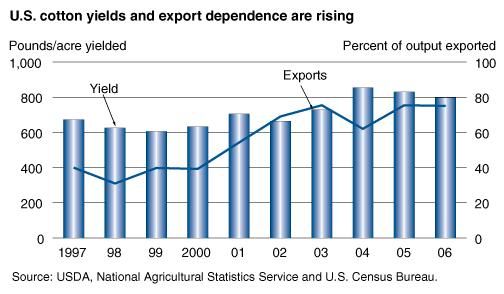

- While demand for U.S. cotton has increased considerably over the last several years, the United States has become an export-dominated market as the domestic textile industry has declined significantly.

This month’s U.S. cotton forecasts for 2010/11 show lower production, higher domestic mill use, and lower ending stocks. The production estimate is reduced 215,000 bales from last month based on USDA’s final Cotton Ginnings report released March 25, 2011. Domestic mill use is raised 100,000 bales, reflecting recent activity. The export estimate is unchanged. Ending stocks are reduced 300,000 bales to a record low 1.6 million, the equivalent of 8 percent of total use. The forecast range for the marketing-year average price received by producers of 81 to 84 cents per pound is raised 1 cent on each end of the range.

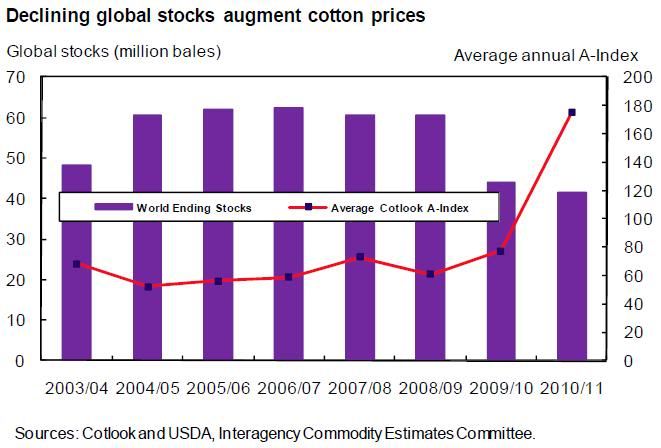

The world cotton forecasts for 2010/11 include lower production and higher consumption, resulting in a 2-percent reduction in ending stocks. World production is reduced about 400,000 bales, based on decreases for the United States, the African Franc Zone, Turkey, and Pakistan, partially offset by an increase for Brazil. World consumption is raised, reflecting increases for Pakistan, the United States, and others, partially offset by a decrease for Brazil. Revisions to world trade include lower exports by Brazil and the African Franc Zone and lower imports by China and Pakistan. Forecast ending stocks of 41.6 million bales are 36 percent of world consumption, which is the smallest stocks-to-consumption ratio since 1993/94.

For the past month, the cotton bale price has hovered near 200 cents per pound. A bale weighs 480 pounds, or 218 kilograms. One 480-pound bale is enough for 215 pairs of jeans. At $2 per pound, this would make the average cost of cotton for each pair of jeans approximately $4.46.

5-year Cotton Price - source:finviz

The U.S. is expected to regain the status as the world's largest cotton exporter and supplier to China this year, but has hit a low stocks-to-use ratio of 8%. Cotton is included in our government's direct payment policy and its production this year may be even more lucrative than the high priced grain markets. U.S. exports have been surging in 2011 to China, Turkey, and Bangladesh.

Cotton demand has something in common with meat demand. That is, as the large populations in the developing nations become more prosperous, especially in China and India, the demand for textiles increases.

While ready-to-wear clothes are available, many Indian women pick cloth they

like and have garments custom made by a local darzi, or tailor.

source: flickr

China, the world's major cotton importer, has announced that they are once again building a cotton reserve. This will encourage cotton production within China by supporting prices.

The expectation is that cotton prices will fall next season, but limitations on seed and equipment limit farmers' ability to ramp up sowing in some places to cash in on the strong market. This is why production is only expected to increase by around 11%, even though prices have doubled over the past year. Cotton rose to $2.197 on March 7, the highest in 140 years of trading in New York. Cotton surged 92% in 2010, the biggest annual gain since 1973. The price advanced 157% in the past 12 months on the S&P GSCI Commodity Index, surpassing silver and coffee gains, which also more than doubled.

Synthetics have grown in use to help even out high cotton prices. Since it takes six months from cotton in the fields to turn-around clothing, today's clothing was made with cotton at half the price of the current market. Polyester is roughly twice as cheap compared with cotton as it was five years ago. Hanes company is starting to use Flax as an added fiber to reduce its cotton expense.

Cotton's stocks-to-use ratio globally may rise to 40-44% next season, though that is well below its 10-year average of 50%. That would be up nicely from this past season's ratio of 37%.

The International Cotton Advisory Committee, a Washington-based 43-member country group, predicts that cotton’s share of the global textile market will shrink to about 30 percent by 2020 from about 37 percent as mills switch to synthetics. However, Jagdish Parihar, managing director of the cotton division at Olam, a Singapore-based trader of farm commodities, predicts that a sustained annual demand growth of 3-4% is a possibility.

K. McDonald