Earlier this month, Reuven Glick released his outlook for the U.S. economy from the Federal Reserve Bank of San Francisco. Below, I've excerpted the parts pertaining to oil prices and commodity prices. Falling labor costs and increasing productivity in the U.S. are making up for inflating commodities while increased demand is coming primarily from the developing nations (in this past decade).

K. McDonald

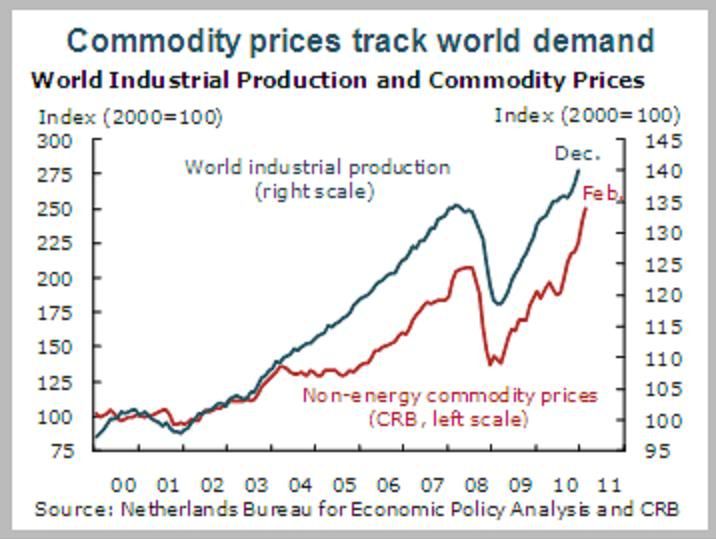

"Global commodity prices have followed global economic activity as measured by world industrial production. Commodity prices fell during the recent recession and rose with the recovery, which increased demand for raw materials, particularly from developing countries such as China. In fact, increased demand from developing countries accounts for most of the increased world demand for commodities such as oil, wheat, and corn over the past decade. In the case of corn, a substantial amount of increased demand also reflects its use in ethanol production.

Commodity price swings have a direct impact on headline inflation through higher costs of energy and food, which account for 14% of overall consumer spending. However, commodity price swings—even double-digit changes—historically have had only a small effect on underlying inflation, which excludes spending on volatile energy and food components. To some extent, this reflects decisions by businesses to adjust profit margins rather than pass through higher costs to customers, particularly when demand is weak.

A more important reason is that for many consumption goods, commodities and raw materials account for only a small part of the overall cost of production, particularly compared with the costs of labor, distribution, and retailing. Moreover, roughly three-fourths of consumer spending is on services such as housing and medical care that do not involve many commodities in production."

"Escalating gasoline prices represent a headwind on consumption by draining purchasing power and undermining consumer confidence.

Higher oil prices pose a particular risk to this outlook by acting as a form of tax on household income. However, most estimates indicate that another similar jump in oil prices likely will shave only a few tenths of a percentage point off GDP growth this year.

Over the past 12 months, overall headline inflation as measured by the personal consumption expenditures price index has risen 1.2%, while core PCEPI has risen 0.8%. We expect recent commodity and energy price surges to raise headline inflation temporarily. We foresee relatively little pass-through to core inflation in 2011 and 2012. The slowly recuperating economy, excess capacity, and well-anchored long-term inflation expectations will keep labor costs low. In fact, with labor productivity continuing to rise, unit labor costs have actually been falling recently.

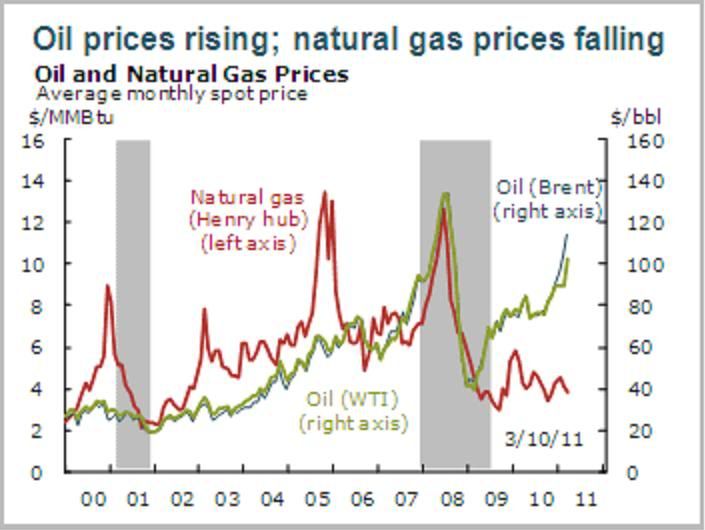

Oil prices have been firming since the global recovery began in 2009, but in recent weeks they have spiked further because of developments in the Middle East and supply uncertainty. Prices of non-energy commodities, including metals, foodstuffs, and textiles, have also risen sharply. However, natural gas prices have remained low as increased production has outpaced demand."

K. McDonald

"Global commodity prices have followed global economic activity as measured by world industrial production. Commodity prices fell during the recent recession and rose with the recovery, which increased demand for raw materials, particularly from developing countries such as China. In fact, increased demand from developing countries accounts for most of the increased world demand for commodities such as oil, wheat, and corn over the past decade. In the case of corn, a substantial amount of increased demand also reflects its use in ethanol production.

Commodity price swings have a direct impact on headline inflation through higher costs of energy and food, which account for 14% of overall consumer spending. However, commodity price swings—even double-digit changes—historically have had only a small effect on underlying inflation, which excludes spending on volatile energy and food components. To some extent, this reflects decisions by businesses to adjust profit margins rather than pass through higher costs to customers, particularly when demand is weak.

A more important reason is that for many consumption goods, commodities and raw materials account for only a small part of the overall cost of production, particularly compared with the costs of labor, distribution, and retailing. Moreover, roughly three-fourths of consumer spending is on services such as housing and medical care that do not involve many commodities in production."

"Escalating gasoline prices represent a headwind on consumption by draining purchasing power and undermining consumer confidence.

Higher oil prices pose a particular risk to this outlook by acting as a form of tax on household income. However, most estimates indicate that another similar jump in oil prices likely will shave only a few tenths of a percentage point off GDP growth this year.

Over the past 12 months, overall headline inflation as measured by the personal consumption expenditures price index has risen 1.2%, while core PCEPI has risen 0.8%. We expect recent commodity and energy price surges to raise headline inflation temporarily. We foresee relatively little pass-through to core inflation in 2011 and 2012. The slowly recuperating economy, excess capacity, and well-anchored long-term inflation expectations will keep labor costs low. In fact, with labor productivity continuing to rise, unit labor costs have actually been falling recently.

Oil prices have been firming since the global recovery began in 2009, but in recent weeks they have spiked further because of developments in the Middle East and supply uncertainty. Prices of non-energy commodities, including metals, foodstuffs, and textiles, have also risen sharply. However, natural gas prices have remained low as increased production has outpaced demand."