photo: flickr

In this post, I have the good fortune of having permission to use the writing of two Ag/Economic experts on the subjects of:

- why people think that speculators drive food commodities

- why speculators, in actuality, do not drive food commodity prices

So, I continued to try to educate myself on the subject, reading Paul Krugman's take, the Naked Capitalism/Paul Krugman Debate, reading Bloomberg and others as they continued to blame speculators, listening to video talks, and the like. Still, I was getting conflicting information and not ready to make a proclamation on this blog.

The first friend who challenged me on this subject linked a Paul Krugman post and told me I should read the Sanders and Irwin paper which Krugman referenced below his post. Imagine my surprise when the third person who contacted me was Irwin himself, whom Krugman cited. I was humbled to have Scott a reader here, but also delighted to have his expertise for consultation.

To present the explanation, I have chosen the writing of Nevil Speer PhD, University of Western Kentucky. He explains it as clearly and simply as I have seen in writing to date. Then, following his article, I have added some critical material given to me from Scott Irwin to help complete the understanding.

K. McDonald

__________________________________

The following is from Agsight March 2011 by Nevil Speer, PhD, MBA of Western Kentucky University:

“Food prices have sparked a media feeding frenzy of late.” That observation from last month’s AgSight stemmed from the seemingly unending stream of headlines about the current inflationary environment. Such widespread media attention is relatively new - the business surrounding agriculture and food production doesn't normally attract much attention. What isn’t new is the finger pointing.

More specifically, the commodity run of late has revived long-standing accusations about speculators. They're the alleged culprits of higher prices and accused of unduly profiting from their respective commodity positions. Meanwhile, the rest of the world suffers the fallout – especially significant in the food arena.

That sentiment was on clear display at a recent meeting of international farm ministers in Berlin. The consortium collectively declaring that, “excessive price volatility and speculation on international agricultural markets might constitute a threat to food security.” And some were individuals were harsher yet; for example French Agriculture Minister Bruno Le Maire: “We don’t want to accept this speculation on agricultural commodities, which…enriches a lot of people but which impoverishes the rest of the planet.” In other words, speculator positions are “excessive” and circumvent underlying fundamentals.

It’s one thing to hear foreign ag ministers condemn the role of speculators in the futures markets but it’s another matter when a market regulator (Bart Chilton, Commissioner, CFTC) does so: “Some people are arguing that we are seeing ‘delinked prices – prices ‘delinked’ from true demand and supply…I’m not an economist. I can’t say what percentage is due to speculation. But it’s easy to find evidence that they are having an impact.” That’s a troubling observation on a number of fronts.

The political rhetoric conveniently avoids market realities. One, futures markets are a zero-sum game: every contract mandates a buyer on one side and a seller on the other (yes, it’s that simple). Hence, hand-wringing about speculative buying is a one-sided venture; there must be an equal value of willing sellers on the other side. Two, in light of simultaneous and balanced price agreements, it’s impossible to assert whether speculators are actually driving the trend or simply chasing it. Lastly, speculators possess no association with the physical product.

Therefore, the only means by which speculative buyers can impact the spot market is to take delivery and remove the physical product from the marketplace. Dr. Craig Pirrong (Professor of Finance and Energy Markets, Univ. Of Houston; streetwiseprofessor.com) summarizes futures markets like this (Regulation, Summer, 2010):

…even if speculation caused prices to go up, that does not necessarily imply that prices were too high as a result. It is possible that speculators recognized that prices were too low (given fundamental information) and that their buying moved prices to the right level…[and] although the speculator may buy, he is almost invariably a seller when a commodity futures contract nears delivery. This would suggest that even if his initial purchase drove up prices, his subsequent sale would drive down prices. Absent some (unexplained) asymmetry in price response to the speculator’s purchases and sales, it is difficult to understand how his actions could affect the prices consumers pay and producers receive.

In other words, placing blame on one side of the equation (non-commercial longs) is misplaced. As alluded above, none of this is really new. Historically, though, the assertions have arisen from the other direction. That is, speculators force prices lower (not higher) with producers being the casualties (not end-users). Charles Geist (Wheels of Fortune: The History of Speculation from Scandal to Respectability) cites a popular 1880's publication entitled, Seven Financial Conspiracies That Have Enslaved the American People. Geist explains the publication’s theme was, “…to show how the average agrarian was at the mercy of the Wall Street crowd that cared only for money, not products.” So either way, the speculator is to blame.

Food prices are driven, like any other market, by supply and demand. Markets work: higher prices occur because of relative scarcity fundamentals: tight supplies amidst strong demand and forecasts for the ongoing continuation of that trend propel the market higher. Simultaneously, price volatility is amplified as scarcity (or at least the perception thereof) becomes more extreme. Moreover, we work in a new reality; money flow occurs faster (24-hour, electronic trading) and with more breadth (globally, across all classes of assets) than ever - that makes for more active markets.

Reining in speculators seems politically expedient. But we live in complex times. Throwing darts becomes perilous when policy makers begin to advocate (and worse yet, actually believe) that speculators should be removed ag / food markets. Such a move would dismantle futures markets. Imagine what the world might look like a without market liquidity, price discovery and risk mitigation; not to mention the inability to establish pricing plans, attract new capital investment and stimulate innovation across the food business. The absence of those influences, facilitated by futures markets, would ultimately lead to less global food security – NOT the other way around. Taking speculators out of the mix would be devastating.

[END Speer Article]

______________________

Next, are Scott Irwin's responses to some questions I posed to him.

First, I asked him why Bloomberg was wrong for blaming speculators for driving oil prices up lately. (His answer applies to food commodities, as well.)

I don’t doubt that speculators are moving from food to oil, but the question remains whether the speculators are following price trends or causing the price trends. The flow of speculators across markets could have a price impact but I would expect it to be temporary in nature and only last a few days at most.

The available research indicates speculators as a group are trend-followers, not trend-makers. Certainly, some speculators are able to anticipate trends and they therefore look like “trend-makers,” but over time this can only be true in a reasonably competitive market if they possess valuable private information or are better at interpreting public information than other traders.

So, to my way of thinking (admittedly very econocentric) the key driver of price trends is changing information about supply and demand prospects. In terms of current events, I believe the price moves generally reflect the best information available about market conditions.

Obviously this is an incredibly dynamic and volatile situation, so there will be large differences in beliefs/perceptions about supply and demand prospects and it is very hard to sort the wheat from the chaff in real time. And when it is so difficult to peer into the future it is tempting to ascribe causality to something that is tangible and measurable---changing positions of speculators.

Next, I asked why wheat prices went up more than 50% the last part of 2010 when supply had remained fairly constant:

In terms of the wheat market specifically last fall, I think the run up made good sense given that there was a truly tight supply in HRW due to production problems in Russia. Looking at the all wheat figures masks what was going at the margin in hard wheat. The other classes had to move in tandem to maintain price relationships.

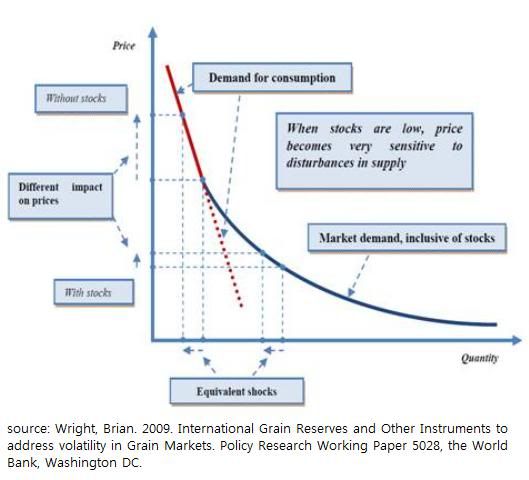

This next statement and graph from Scott is most critical to understanding the concept:

In addition, the wheat price move also reflected the fundamental “non-linearity” in the relationship between inventories and price. The figure above, drawn from Wright (2009), illustrates this point. Note that a given reduction in quantity due a to supply and/or demand shock will have a much larger impact on price when starting with a low quantity (inventories) compared to when starting with a high quantity. It also implies that relatively minor reductions in quantity can result in very large increases in price when the market supply/demand balance is especially tight. This is a key point that I think is missed by many people.

[END Irwin answer]

_______________________________

For further references, see Dwight Sanders and Scott Irwin's most recent paper on this subject here: Index Funds, Financialization, and Commodity Futures Markets.

Paul Krugman: Commodities, This Time is Different; and Nobody Believes in Supply and Demand.

Note that Scott Irwin PhD, University of Illinois, has a newly revised and updated agricultural news blog site, "Farm Doc Daily" which you may access from the left sidebar here.