This post includes highlights from the Chicago, Kansas City, Minneapolis, and Dallas Federal Reserve District farmland price reports.

The general overall trends are that prices have gone up fairly significantly, outlooks are for further price increases, and land sales volumes have been limited, though an increased amount is expected to sell in the final quarter of 2010. The strongest prices this quarter are from intensive grain commodity producing acres.

(This is the first in my series of November 2010 farmland price update posts.)

~~~~~~~~~~~

SEVENTH DISTRICT: CHICAGO

(Iowa and most of Illinois, Indiana, Michigan, and Wisconsin)

Percent Change in dollar value of "good" farmland

Top: July 1, 2010 to October 1, 2010

Bottom: October 1, 2009 to October 1, 2010

Illinois +3% — +8%

Indiana +2% — +11%

Iowa +6% — +13%

Michigan +3% — +10%

Wisconsin +1% — +3%

Seventh District +3% — +10%

~~~~~~~~~~~

TENTH DISTRICT: KANSAS CITY

(Colorado, Kansas, Nebraska, Oklahoma, Wyoming, northern New Mexico, and Western Missouri)

Quotes from a few of the region's bankers:

source: 10th District--Kansas City

~~~~~~~~~~~

NINTH DISTRICT: MINNEAPOLIS

(Minnesota, Montana, North Dakota, South Dakota, twenty-six counties in northwestern Wisconsin, and the Upper Peninsula of Michigan)

~~~~~~~~~~~

ELEVENTH DISTRICT: DALLAS

(Texas, northern Louisiana, and southern New Mexico)

~~~~~~~~~~~

The general overall trends are that prices have gone up fairly significantly, outlooks are for further price increases, and land sales volumes have been limited, though an increased amount is expected to sell in the final quarter of 2010. The strongest prices this quarter are from intensive grain commodity producing acres.

(This is the first in my series of November 2010 farmland price update posts.)

SEVENTH DISTRICT: CHICAGO

(Iowa and most of Illinois, Indiana, Michigan, and Wisconsin)

Percent Change in dollar value of "good" farmland

Top: July 1, 2010 to October 1, 2010

Bottom: October 1, 2009 to October 1, 2010

Illinois +3% — +8%

Indiana +2% — +11%

Iowa +6% — +13%

Michigan +3% — +10%

Wisconsin +1% — +3%

Seventh District +3% — +10%

- Propelled by rising agricultural prices, farmland values jumped 10 percent in the third quarter of 2010 from a year ago in the Seventh Federal Reserve District.

- The value of “good” agricultural land rose 3 percent relative to the second quarter of 2010.

- Loan repayment rates improved in July through September of this year compared with the same period of 2009.

- Interest rates on agricultural operating and real estate loans dropped to the lowest values recorded in history of the survey.

- Farmland values in Iowa were up the most, with a year-over-year increase of 13 percent for the third quarter of 2010.

- Indiana and Michigan followed closely with yearover-year increases of 11 percent and 10 percent, respectively.

- Illinois had a slightly smaller increase of 8 percent, while Wisconsin, at 3 percent, had the slowest growth in farmland values from a year ago.

- The District’s agricultural land values gained 3 percent from the second quarter to the third quarter of 2010.

- Farmland demand for recreational purposes has lagged and contributed to wider gaps in selling prices between more productive cropland and poorer quality land.

- Wisconsin was the only state with a drop in loan repayment rates, although this decrease was much smaller than a year ago.

- For the District, 13 percent of the bankers forecasted more forced sales or liquidations and 25 percent expected fewer.

- All strength in (non-real-estate loan) volumes was concentrated in Illinois and Iowa. Respondents anticipated expanded volumes for operating loans (15 percent more forecasted increases rather than decreases), farm machinery loans (25 percent), grain storage construction loans (7 percent), Farm Service Agency guaranteed loans (10 percent), and farm real estate loans (14 percent).

TENTH DISTRICT: KANSAS CITY

(Colorado, Kansas, Nebraska, Oklahoma, Wyoming, northern New Mexico, and Western Missouri)

- District farmland values hastened their climb in the third quarter of 2010 with rising farm income and robust demand for farmland.

- More district bankers reported higher farm income as many producers marketed their crops at these elevated prices.

- With a return to profitability for the livestock sector, ranchland values rose as well, recovering from declines earlier this year.

- Robust demand by farmers was still the primary driver in district farm real estate markets, though investor interest in good quality farmland remained high. District bankers noted that nonfarm investors typically expected a 5 percent or better rate of return on farmland purchases.

- With incomes climbing in the third quarter, farm credit conditions improved.

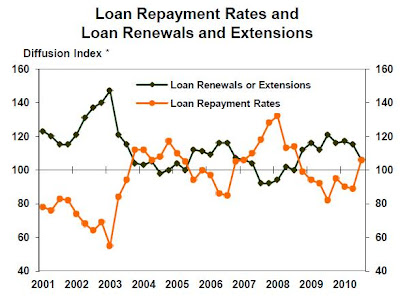

- More district bankers noted higher loan repayment rates and fewer loan renewals and extensions.

- Average farm loan interest rates fell to their lowest levels since the survey began in 1976 and collateral requirements eased.

- Farm loan demand was steady and district bankers indicated an ample supply of funds available for qualified borrowers.

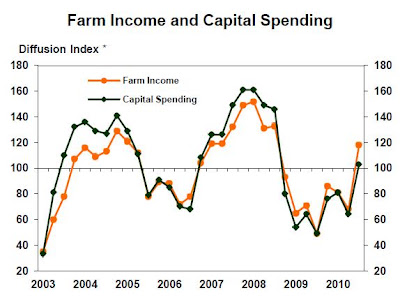

- Survey respondents reported a significant rebound in capital spending, especially for crop equipment and grain storage bins.

- District farmland values have climbed steadily since a slight dip in value during the third quarter of 2009.

- Farmland values have risen each of the last four quarters, posting the strongest annual value gains since 2009.

- Compared to the previous year, the value of irrigated and nonirrigatedcropland rose 9.6 and 6.4 percent, respectively.

- District cropland value gains were driven by Nebraska and Kansas, major crop producing states where farm income was up substantially in the third quarter.

- Profits in the livestock sector continued to rise, which helped lift year-over-year ranchland values by 4.3 percent.

- Annual farmland cash rental rates were also up, but the gains were not quite as dramatic.

- Compared to last year, cash rental rates were about 5.0 percent higher for cropland and around 2.0 percent higher for ranchland.

- Rising farmland values were also driven by strong demand for good quality farmland from both farmers and nonfarm investors.

- Bankers reported that investors expected an average rate of return between 5 and 6 percent for farmland investments.

- After a two-year decline in the supply of farms offered for sale, a number of bankers mentioned that farm owners who were considering selling may market their properties before year-end to take advantage of current elevated prices and avoid potentially higher capital gains taxes in 2011.

- District farm incomes strengthened substantially in the third quarter, driven by booming commodity prices. Since June, crop prices have risen on prospects of lower than expected global and U.S. grain supplies.

- Higher prices helped boost the farm income index to its highest level in two years, with additional gains expected over the next three months.

- Good weather conditions across the district facilitated an early harvest with yields less than early estimates but slightly better than their five-year average.

- Livestock prices generally held steady, but higher feed costs narrowed profit margins and could dampen the rebound in the livestock sector.

- Stronger farm incomes spurred producers to raise their capital spending on crop equipment and grain storage bins.

- Farm credit conditions also improved with stronger incomes. During the third quarter, the loan repayment index rose past 100 for the first time in two years, and the index of loan renewals and extensions fell.

- Collateral requirements eased and referrals to nonbank credit agencies held steady. Farm interest rates fell further, reaching a new survey low of 6.7 percent for operating loans and 6.4 percent for farm real estate loans.

- During the third quarter, the funds availability index rose to a historically high level, indicating agricultural banks had plenty of funds available for qualified borrowers.

- After fluctuating widely over the past three years, demand for farm loans was essentially flat. Bankers expected only modest farm loan growth over the next three months as higher farm incomes may lessen the need for financing.

Quotes from a few of the region's bankers:

- Land fever is running rampant. It appears that the combination of low investment returns for financial assets and the generally strong farm sector has spurred a voracious appetite for agricultural land.---NE Kansas

- Many investors would rather have farmland than low yields on bank deposits.---SW Oklahoma

- I expect there will be some profit taking in farm real estate.---Western Kansas

source: 10th District--Kansas City

NINTH DISTRICT: MINNEAPOLIS

(Minnesota, Montana, North Dakota, South Dakota, twenty-six counties in northwestern Wisconsin, and the Upper Peninsula of Michigan)

- Farmland prices in the five states in the district were up 9 percent in the third quarter just ended, compared with the third quarter in 2009.

- Irrigated farmland prices were up 6.8 percent and ranch land was up 3 percent in the same period.

- Minnesota was the best performer, with non-irrigated farmland up 12.3 percent in the third quarter over a year earlier.

- Prices for North Dakota’s dry land farm acres were up 10 percent in the quarter over 2009’s third quarter; irrigated acres were up 3.6 percent in price and ranch land up 4.7 percent.

ELEVENTH DISTRICT: DALLAS

(Texas, northern Louisiana, and southern New Mexico)

- Current land values are stable or slightly up, although land sales remain subdued.

- Some weakness in farm lending persists, although loan repayment rates and requests for renewals or extensions stabilized in the third quarter.

- Demand for loans continues to wane, with one quarter of bankers noting a falloff in demand compared with 17 percent reporting an increase.

- However, demand for operating and crop storage loans is stronger than last quarter and much stronger than a year ago, likely due to robust agricultural production.

- Cattle profits have improved as cattle coming out of the feed yard are now making $50 to $100 per head.... Operating expenses were up slightly more than expected mainly due to increased fertilizer and irrigation costs.---Northern High Plains Texas

- Many producers are hoping to reduce debt going into 2011. Land prices are holding firm, but few properties are selling. There are very few metroplex buyers right now, and land is too expensive for farmers and ranchers to purchase.---Northern Low Plains Texas

- Oil and gas leasing and income are still the major driving force behind the area economy. Rural farm and ranch sales are very limited. Listings are way down as landowners wait out oil- and gas-related activity. Various real estate tracts in the surrounding areas and in the Eagle Ford Shale deposits are receiving leases from oil and gas companies in excess of $1,500 per acre and up to $4,000 per acre. This in turn has increased the asking price on much of the farm and ranch land to highs exceeding their value. Because of this, very little property is being purchased. The primary areas are in North Bee, Kennedy, Jim Wells, Live Oak and Goliad Counties. Cattle numbers are down. The trend is toward reduced stocking rates to help manage input costs.---Central Texas